This post may contain affiliate links, which means if you click through and purchase something using my links, I receive a small commission. You can click here to read my disclosure policy ? Thank you!

The last time I was apartment-hunting, I was terrified about being homeless. While I could have lived with my parents, they lived in an age-restricted community, which meant I couldn’t stay there for a long period of time. I didn’t have much money and, worst of all, my credit was really bad.

The last time I was apartment-hunting, I was terrified about being homeless. While I could have lived with my parents, they lived in an age-restricted community, which meant I couldn’t stay there for a long period of time. I didn’t have much money and, worst of all, my credit was really bad.

This was a big deal because credit, and credit scores, can have a big impact on so many things in our lives, including where we can live, to how much we might pay for a car loan or mortgage. Eventually, I convinced two friends to join up with me and we ended up splitting an apartment – but it was dicey for a while!

Back then, I had no idea how I could monitor my credit. I knew I could get a free, annual credit report from the three credit bureaus, but I didn’t know what the information meant or what my score actually was. The whole topic of “credit reports and scores” was nebulous, confusing – and hard.

Eventually I ended up improving my credit score immensely – I now have excellent credit and don’t worry too much about my report or score. But that’s only possible because I check my credit every single month – for free. I wouldn’t be anywhere near as informed without free credit reporting services, like Credit Sesame. I’ll cover what Credit Sesame is, what it shows you and and how you can use it!

Not really sure how your credit works? How to go from ‘no credit’ to excellent credit here!

What is Credit Sesame?

Credit Sesame is a company that provides free credit monitoring, whenever you want – did I mention it’s free? Credit Sesame pulls your information from TransUnion, one of the credit bureaus.

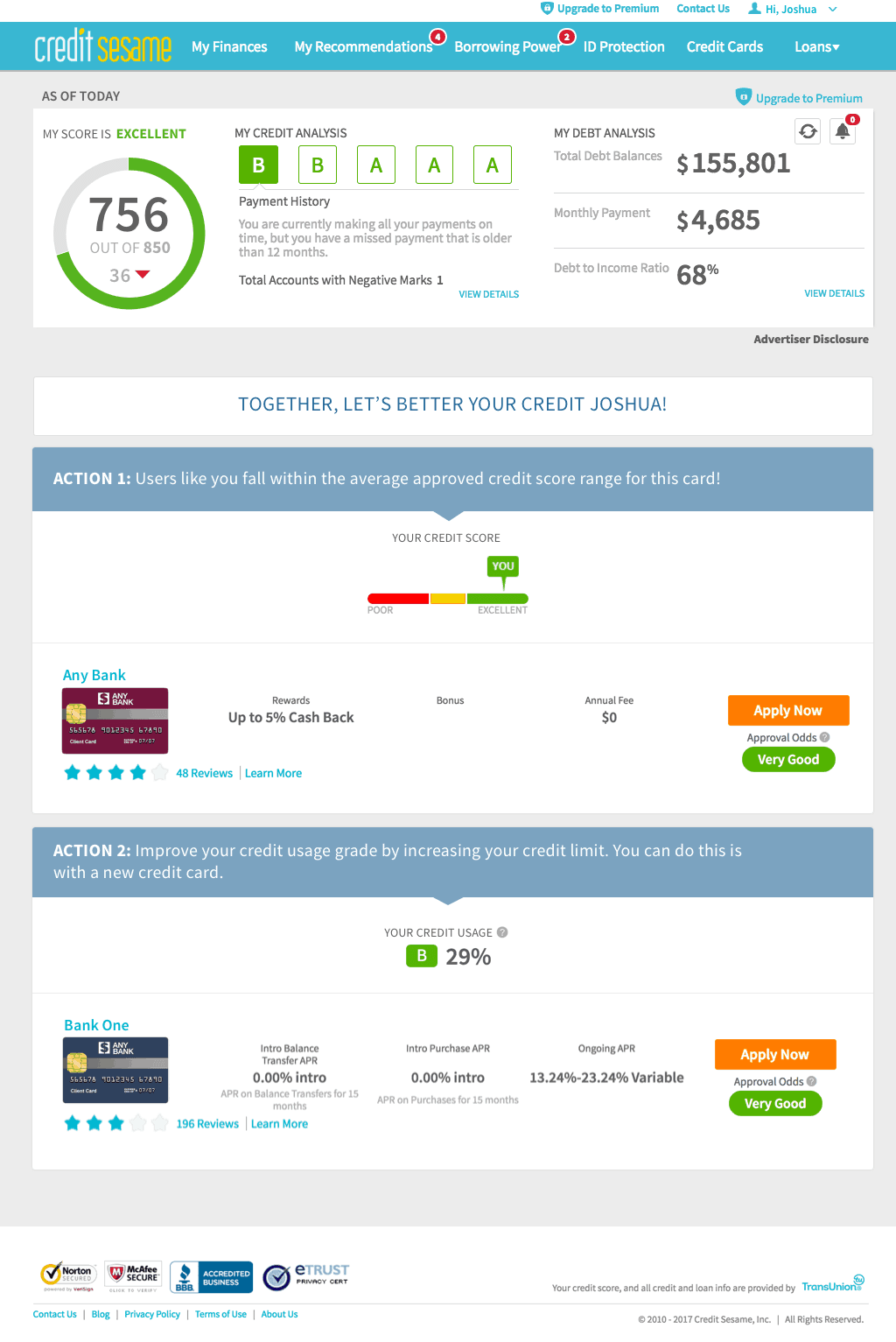

When you first pull up Credit Sesame, it looks a lot like the example to the left (only with your information, of course). It gives you your current store, information about your debt, monthly payment, action steps and goals (if you choose to set them).

With Credit Sesame, you can also sign up for credit monitoring alerts. It’s helpful – and legit.

Recently, my husband and I applied for a mortgage, and almost right away, Credit Sesame sent me an alert notifying me of activity related to my credit. I knew about it, but if I hadn’t, I would have been able to address the situation right away!

What else do you get with a free Credit Sesame account?

- Free advice: Credit Sesame analyzes your loans and credit card debt every day as the market changes, and if there’s a better loan option that saves you money, they’ll alert you.

- Free tracking and alerts: CS updates your credit score and loan information every month, then creates easy-to-use trending graphs so you can track how you’re doing.

- Free home value estimates: CS updates the estimates of your home value and the amount of home equity you’ve built up every month.

- Free financial goal-setting: Credit Sesame helps you set your own financial goals – like refinancing a home, borrowing money or buying a house – and alert you when we find an offer that meets your goals and saves you the most money on interest.

Why Should I Be Concerned About My Credit Score?

Your credit score basically shows your ‘credit worthiness’, which translates to: are you someone a bank should loan money to? Do you pay your bills on time, and should an apartment company or landlord trust that you will pay them on time?

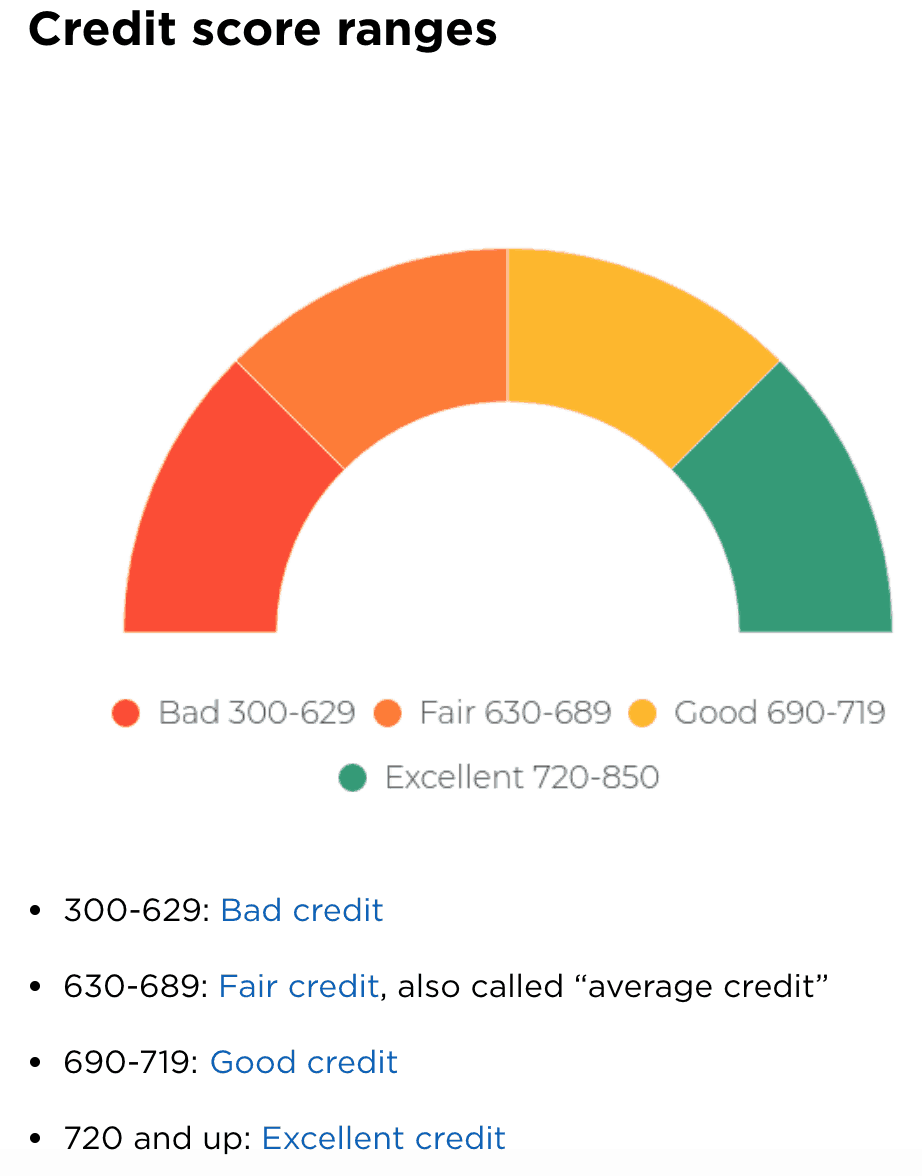

If you have bad credit, don’t panic! It doesn’t mean you’re a bad person or that you will never get credit – it just means that you’ll have to work twice as hard as someone with good or excellent credit. Here are the tiers to determine how your credit score might stack up [image and description from NerdWallet!]:

If you have a lower score (anything below good) you can generally expect to pay higher interest rates on car loans or mortgages. In addition, some apartment complexes or landlords may require you to put more money down as a deposit (or pay the first and last month’s rent) in order to “prove” you will pay on time.

In fact, NerdWallet found that:

For instance, someone with FICO scores in the 620 range would pay $65,000 more on a $200,000, 30-year mortgage than someone with FICOs over 760, according to data gathered by Informa Research Services.

At the other end of the scale, borrowers with scores above 750 or so have many options, including the ability to qualify for 0% financing on cars and 0% interest credit cards.

Overall, it sucks to have a bad credit score, but all is not lost if you have a bad credit score! I once had a credit score in the 600s – it was bad! However, it’s not impossible to improve your score.

How to Improve Your Credit Score

First, sign up for a free credit monitoring service like Credit Sesame. Make sure your credit report accurately depicts your financial life: are the debts listed your debt? If not, you could be the victim of fraud and you’ll want to get that fixed immediately!

First, sign up for a free credit monitoring service like Credit Sesame. Make sure your credit report accurately depicts your financial life: are the debts listed your debt? If not, you could be the victim of fraud and you’ll want to get that fixed immediately!

Once you’ve cleaned up any issues (or if there were none), it’s time to focus on steadily paying off debt and making sure you make all your payments every month.

- List out everything you owe monthly – include student loan, credit card payments, your rent/mortgage costs, car loan – anything you must pay monthly (this does not include food or entertainment).

- Add up everything you make per month – include your regular, full-time (or part time) job and any side hustles you do, plus any other income you bring in.

- Subtract your monthly costs from your monthly income. If your income is higher than your expenses, great! Just make sure to pay your bills on time, focus on steadily paying off your debt, and your credit score will improve.

If your monthly income is not higher than your monthly costs, this is probably why you don’t have a great credit score. If you can’t pay your bills every month, you will get “dinged” by the companies you are not paying, which gets reported to credit agencies and is reflected on your credit score. Focus on earning more money, negotiating your bills down if possible (companies would rather have you pay something rather than nothing, so call and ask!), and making on-time payments.

As you work on improving your credit score, be sure to use and check in on a free credit monitoring service, like Credit Sesame, to stay on track.

Commonly Asked Credit Sesame Questions

Is Credit Sesame Safe?

Yes – Credit Sesame uses bank-level security practices, encryption and firewalls.

How Often Does Credit Sesame Update My Credit Score?

Like many other companies that provide your credit score, Credit Sesame updates credit scores monthly. Plus, according to Credit Sesame, “[we will] show you how it’s trending over time. This monthly check won’t affect your credit score. Note that we don’t provide a full credit report detailing all of your payments and loan activities; we only provide the score.”

Will Credit Sesame’s Automatic Pull of My Credit Score Lower My Credit Score?

According to Credit Sesame, “Never! Because we pull your credit score for your own personal information on a monthly basis and don’t share it with lenders, this results in what is called a “soft inquiry.” Unless you apply for a loan, your credit score will not be impacted.”

Is Credit Sesame Really Free?

Yes, Credit Sesame is 100% free to you! They earn a small fee from banks, but only if you decide to apply for and close on a loan, so it’s in their best interested to find you the best match based on your needs. What else does Credit Sesame offer?

- Free advice: We analyze your loans and credit card debt every day as the market changes, and if there’s a better loan option that saves you money, we alert you.

- Free tracking and alerts: We update your credit score and loan information every month, then create easy-to-use trending graphs so you can track how you’re doing.

- Free home value estimates: We update the estimates of your home value and the amount of home equity you’ve built up every month.

- Free financial goal-setting: We help you set your own financial goals – like refinancing a home, borrowing money or buying a house – and alert you when we find an offer that meets your goals and saves you the most money on interest.

How is Credit Sesame Different from Credit Karma?

You’ve probably heard of Credit Karma from TV – in the commercials, Credit Karma is highlighted as a free way to check your credit score. And it is!

Like Credit Sesame, Credit Karma offers a free credit monitoring service where you can access your scores and credit reports. You can also sign up for free credit alerts, email alerts, and identity theft tracking and protection. One difference between Credit Karma and Credit Sesame though is CK uses TransUnion and Equifax to determine your estimated score.

In addition, Credit Karma also offers a free credit simulator, which takes into account all your credit information, then let’s you visualize what effect different moves you can make impact your score. For example, if you’re deciding between which of two debt pay offs will have a greater impact on your score, you can analyze this information on Credit Karma. You can’t do this (yet!) with Credit Sesame.

Which Free Credit Service is Best?

In the end, there’s no one right answer to the question “which free credit service is the best?” But this time, that’s a good thing! If you want to monitor your credit score, especially if you are planning on applying for a mortgage, apartment, new credit card, or other type of loan, you want to be aware of your credit report, what “bad things” are on it (if any) and how you can improve your score.

You can get started with Credit Sesame today here.

Have you tried Credit Sesame or Credit Karma? Let me know which one you prefer in the comments!